Australian retailers are facing the fight of their life in 2020. Consumer confidence slumped for a period, job losses have soared, and spending behaviour has been tipped on its head. But it’s also been extremely volatile across the sector – many retailers have benefited from stockpiling and a shift towards at-home spending, while others have faced significant drops in demand. The easing of restrictions and large fiscal stimulus program provide some support, but retail is likely to face headwinds on the long recovery path ahead.

Retail Forecasts is produced quarterly and provides analysis of current retail spending and important changes to the economic drivers that influences this. According to Deloitte Access Economics’ latest quarterly Retail Forecasts subscriber report for Q2 2020:

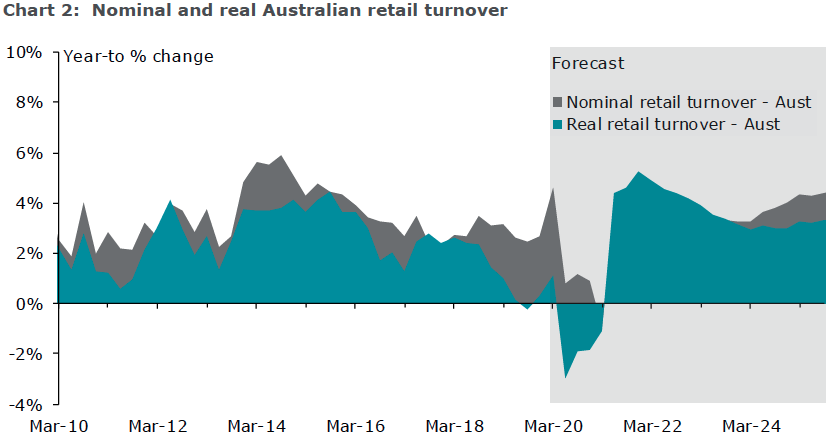

- Real retail turnover growth is expected to fall 1.4% in 2020, making it the worst year on record

- After a surge in growth over the March quarter, retail spending is expected to contract by 4.0% in the June quarter as the COVID-19 outbreak and associated restrictions limit spending

- There have also been significant swings in consumer ability and willingness to spend during 2020, and those swings may continue as the year goes on.

Deloitte Access Economics partner, and Retail Forecasts principal author, David Rumbens, said: “2020 has been a tumultuous year for retailers. We’re not even halfway through, but across the whole sector we expect calendar 2020 to register a record breaking fall in real retail sales.

“But while the average is dire, there may not be many retailers performing at the average – many will fare much worse, while supermarkets, pharmacies and hardware, amongst others, have been experiencing a golden run.

“Consumer willingness to spend will likely be buffeted by a number of different factors, meaning that one month’s trading experience may be a terrible guide to how the year as a whole pans out.

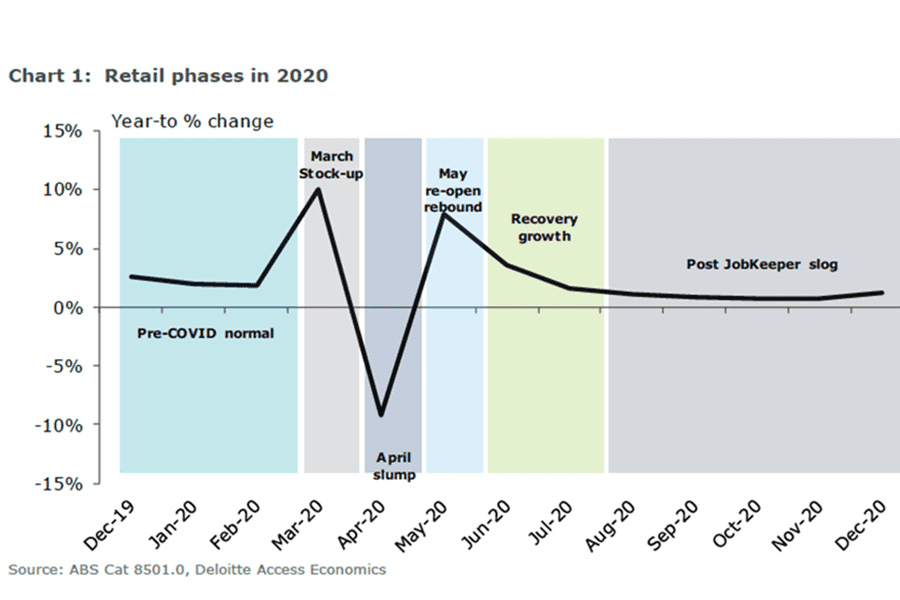

Rumbens says that “rather than one dominant economic theme, we expect six phases to retail spending in 2020.”

1. A pre-COVID normal

Remember January/February? Hardly normal, as the country was dealing with devastating bushfires, and some borders were starting to close. However, for most retailers trading was in a familiar pattern with modest growth from month-tomonth.

2. March stock-up

As COVID led to widespread restrictions, consumers entered a massive stocking-up cycle, with the extra spending on essentials masking a sharp decline in much discretionary spending. This culminated in the strongest monthly growth in retail sales on record.

3. April slump

The stock-up phase tapered off, so supermarket and related spending came back down, while the downturn in discretionary spending (particularly cafes/restaurants and apparel) only got worse. The result? The worst fall in monthly Australian retail sales on record.

4. May re-open rebound

As health concerns abated and consumers were given the green light to go back to shopping centres, retail spending appeared to have once again picked up sharply. This was helped by some pent-up demand, and a lot of government support, cushioning the blow which might otherwise have been seen on consumer incomes.

5. Recovery growth

Tempering the re-opening frenzy, this will be a ‘COVID normal’ period, where sales are buoyed by an improving economy (picking up from a very deep trough), and which continues to benefit from income support measures (JobKeeper, deferral of mortgages, access to super etc.).

6. Post JobKeeper slog

September is already flashing red for many retailers as the month for the intended end to JobKeeper, and therefore the significant support many businesses (including retailers of course) have been receiving. That may see the last phase for retail in 2020 as a fairly sombre one, leaving many retailers to dream of the support they received when COVID was at its peak.

“As we move from re-open rebound in May to recovery growth in June, consumers are re-opening their wallets, if remaining somewhat cautious. Combined with the very deep April slump, this is likely to result in a 4.0% drop in spending in the June quarter, before a fragile recovery through the second half of the year.”

The recovery path for retail spending was precarious. “Short-term risks from rising unemployment and reduced willingness to spend will linger, especially as fiscal stimulus programs are unwound in September,” said Rumbens.

“More worrying is the longer-term risk from weak population growth. Migration has been an important support for retail spending over the past decade, but with borders closed there is potential for this tailwind for growth to turn into a headwind.”